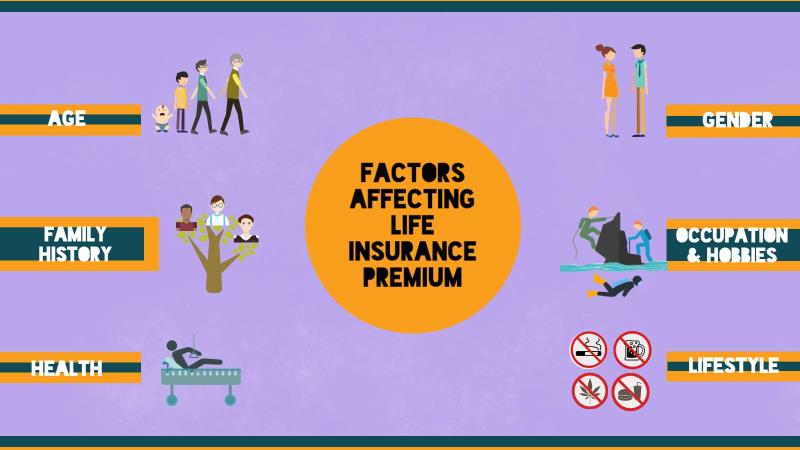

The insurance industry is experiencing a significant transformation driven by emerging trends and technologies. In this article, we explore the future of insurance, examining the innovative solutions and technologies that are reshaping the industry. From artificial intelligence and blockchain to telematics and personalized policies, we delve into the advancements that are revolutionizing the way insurance is provided, purchased, and managed.

Artificial Intelligence (AI) and Machine Learning AI and machine learning are revolutionizing the insurance industry by enabling insurers to automate processes, enhance underwriting accuracy, and improve customer experience. We discuss how AI is being used for risk assessment, claims processing, chatbots for customer service, and fraud detection. These technologies are streamlining operations and enabling insurers to deliver more personalized and efficient services. Internet of Things (IoT) and Telematics The Internet of Things (IoT) is connecting devices and enabling insurers to gather real-time data for risk assessment and personalized pricing. We explore how telematics devices in vehicles and wearables are collecting data on driving behavior, health, and property conditions. This data allows insurers to offer usage-based insurance, incentivize safer behaviors, and optimize coverage. Blockchain Technology Blockchain technology is transforming insurance by enhancing security, transparency, and efficiency in transactions. We discuss how blockchain is being used for policy administration, claims management, and reducing fraudulent activities. The decentralized nature of blockchain ensures data integrity and simplifies the verification process, improving trust among insurers, customers, and other stakeholders. Personalized Policies and Usage-Based Insurance Insurers are shifting towards personalized policies based on individual risk profiles and behaviors. We explore the rise of usage-based insurance, which takes into account real-time data from connected devices. This approach allows insurers to tailor coverage and pricing to the specific needs and behaviors of customers, fostering a fairer and more customized insurance experience. Insurtech Startups and Collaboration Insurtech startups are disrupting the traditional insurance landscape by offering innovative solutions and customer-centric services. We discuss the rise of digital platforms that simplify insurance processes, provide on-demand coverage, and offer peer-to-peer insurance models. Additionally, we explore the growing trend of collaboration between traditional insurers and insurtech startups, enabling incumbents to leverage new technologies and stay competitive. Big Data and Predictive Analytics The abundance of data available to insurers is reshaping risk assessment and pricing models. We explore how big data and predictive analytics are being used to analyze customer data, identify patterns, and make more accurate predictions. This allows insurers to proactively manage risks, prevent losses, and offer personalized products and services. Enhanced Customer Experience Customer experience is at the forefront of the insurance industry's transformation. We discuss the importance of digital channels, self-service options, and personalized interactions. Insurers are leveraging technologies such as AI-powered chatbots and mobile apps to provide 24/7 access, personalized recommendations, and faster claims processing, improving overall customer satisfaction. Regulatory and Ethical Considerations As the insurance industry evolves, there are regulatory and ethical considerations that need to be addressed. We explore topics such as data privacy, cybersecurity, fairness in algorithmic decision-making, and ensuring that vulnerable populations have access to affordable coverage. Balancing innovation with responsible practices is crucial to maintain trust and ethical standards within the industry. Conclusion The future of insurance is being shaped by emerging trends and technologies that are transforming the way insurance is provided and experienced. From artificial intelligence and IoT to blockchain and personalized policies, these advancements are enhancing efficiency, accuracy, and customer satisfaction. As insurers embrace these innovations, they must also navigate regulatory and ethical considerations to ensure responsible and inclusive practices. The future of insurance holds great potential for a more customer-centric, data-driven, and digitally-enabled industry that offers tailored coverage, faster claims processing, and enhanced risk management capabilities. Network Zooporn.blue Zinro.net Yiwu.0579.com Xneox.com Zerocarts.com Wikidot.com Warpradio.com Topkam.ru Thumbnailworld.net Testron.ru Taskmanagementsoft.com Tagirov.org Storyme.app Searchdaimon.com Rentv.com Reefcentral.com Redcruise.com Puurconfituur.be Phpooey.com Openherd.com Myriad-online.com Muppetsauderghem.be Mientaynet.com Krimket.ro Jkes.tyc.edu.tw

0 Comments

Natural disasters such as hurricanes, earthquakes, floods, and wildfires can cause significant damage to your home and property. Having adequate insurance coverage is essential to protect your investment and ensure financial stability during challenging times. In this guide, we will provide you with essential tips for insuring your home against natural disasters, allowing you to weather the storm with confidence.

Understand Your Risks Start by understanding the natural disaster risks specific to your geographic location. Research the history of natural disasters in your area and assess the likelihood and severity of potential events. This will help you determine the types of coverage you need to protect your home. Review Your Homeowner's Insurance Policy Review your existing homeowner's insurance policy to determine the extent of coverage for natural disasters. Standard homeowner's insurance may not cover certain types of natural disasters, such as floods or earthquakes. If necessary, consider purchasing additional coverage or endorsements to address these specific risks. Purchase Flood Insurance Flooding is one of the most common and costly natural disasters. Standard homeowner's insurance policies typically do not cover flood damage. To protect your home, consider purchasing a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private insurer. Assess your flood risk based on FEMA flood zone maps. Consider Earthquake Insurance If you live in an earthquake-prone area, consider purchasing earthquake insurance. Standard homeowner's insurance policies typically exclude earthquake damage. Earthquake insurance can help cover the cost of repairs or rebuilding in the event of an earthquake-related disaster. Evaluate Windstorm Coverage In regions prone to hurricanes or strong windstorms, ensure your homeowner's insurance policy includes coverage for windstorm damage. Some policies may have specific deductibles or limitations for windstorm-related claims. Review your policy carefully and consider purchasing additional coverage if needed. Document Your Property Take inventory of your belongings and document the condition of your property through photographs or video. This will be invaluable in the event of a natural disaster and will help you file accurate insurance claims. Store this documentation in a safe place, such as a cloud-based storage system or a secure off-site location. Review Coverage Limits Regularly review the coverage limits on your homeowner's insurance policy to ensure they align with the current value of your home and belongings. Keep in mind that the cost of rebuilding or repairing your home after a natural disaster may be higher than anticipated due to increased demand for labor and materials. Consider Replacement Cost Coverage When insuring your home, opt for replacement cost coverage instead of actual cash value coverage. Replacement cost coverage will reimburse you for the full cost of rebuilding or repairing your home without deducting depreciation. This ensures you can fully recover from a natural disaster without incurring significant out-of-pocket expenses. Understand Policy Deductibles Be aware of the deductibles associated with natural disaster coverage. Some policies have separate deductibles specifically for natural disasters. Ensure you understand the deductible amounts and any requirements for deductible payment in the event of a claim. Consult with an Insurance Professional Seek guidance from an insurance professional with expertise in natural disaster coverage. They can help assess your specific risks, evaluate your current coverage, and recommend appropriate insurance options to adequately protect your home. Conclusion Insuring your home against natural disasters is crucial for protecting your investment and ensuring financial stability. By understanding your risks, reviewing and adjusting your homeowner's insurance policy, purchasing additional coverage for flood or earthquake risks, documenting your property, reviewing coverage limits and deductibles, considering replacement cost coverage, and seeking professional advice, you can weather the storm and have peace of mind knowing that your home is adequately insured against natural disasters. Best Site Closingbell.co Book.douban.com Blogranking.fc2.com Bing.com Bigmarty.com Bel-kot.com Bbs.pku.edu.cn Bavaria-munchen.com Zooporn.blue Zinro.net Yiwu.0579.com Xneox.com Zerocarts.com Wikidot.com Warpradio.com Topkam.ru Thumbnailworld.net Testron.ru Taskmanagementsoft.com Tagirov.org Storyme.app Searchdaimon.com Rentv.com Reefcentral.com Redcruise.com  Insurance policies are often filled with complex jargon and fine print, making it challenging for policyholders to fully understand their coverage. In this guide, we will help you decode insurance jargon and navigate the fine print, empowering you to make informed decisions about your insurance policies.

Key Insurance Terminology Familiarize yourself with common insurance terms and their meanings. Understand terms such as premiums, deductibles, coverage limits, exclusions, endorsements, subrogation, policyholder, insured, and insurer. By understanding these terms, you can better comprehend the language used in your insurance policy. Declarations Page Review the declarations page, which provides an overview of your policy details. Understand how to interpret information such as policy effective dates, insured parties, coverage limits, deductibles, and premium amounts. This page serves as a snapshot of your policy and sets the foundation for understanding the fine print. Insuring Agreement The insuring agreement outlines the coverage provided by the insurance policy. Pay close attention to this section as it defines the scope of protection, including the specific risks covered. Understand the language used to describe coverage, including any conditions or limitations mentioned. Exclusions and Limitations Exclusions are specific situations or risks that are not covered by the insurance policy. These exclusions can vary depending on the type of insurance. Take the time to identify and understand the exclusions listed in your policy. Likewise, be aware of any limitations on coverage, such as sub-limits or restricted coverage for certain items or events. Conditions and Requirements Insurance policies often have specific conditions and requirements that must be met for coverage to apply. This can include maintaining certain safety measures, providing timely notice of claims, or cooperating fully with the insurer during the claims process. Familiarize yourself with these conditions to ensure you fulfill your obligations as a policyholder. Endorsements and Riders Endorsements and riders are modifications or additions to the standard policy terms. They can expand or restrict coverage based on your specific needs. Carefully review any endorsements or riders included with your policy to understand how they impact your coverage. Policy Renewal and Cancellation Pay attention to the fine print regarding policy renewal and cancellation. Understand the terms and conditions surrounding the renewal process, including any rate adjustments or changes in coverage. Similarly, be aware of the circumstances under which the insurer can cancel or non-renew your policy. Claims Process Familiarize yourself with the claims process outlined in your policy. Understand the steps to follow when filing a claim, including the required documentation, timelines, and communication channels. Be aware of any policy provisions that may impact the claims settlement process. Seek Clarification If you encounter unfamiliar terms or unclear provisions in your policy, don't hesitate to seek clarification. Reach out to your insurance agent or insurer to ask questions and request further explanation. It's essential to have a clear understanding of your coverage to ensure you're adequately protected. Review and Update Regularly Insurance policies can evolve over time, and it's crucial to review and update them regularly. Keep track of changes in your circumstances and assets, and consult with your insurance professional to ensure your coverage remains appropriate and up to date. Conclusion Decoding insurance jargon and understanding the fine print of your policy can seem daunting, but it is crucial for maximizing your coverage and protecting your interests. By familiarizing yourself with key insurance terminology, reviewing the declarations page, understanding the insuring agreement, identifying exclusions and limitations, fulfilling policy conditions and requirements, reviewing endorsements and riders, knowing the policy renewal and cancellation terms, understanding the claims process, seeking clarification when needed, and regularly reviewing and updating your policies, you can navigate the complexities of insurance with confidence. Remember, your insurance agent or insurer is a valuable resource and can provide guidance to ensure you fully comprehend your coverage. Network Zooporn.blue Zinro.net Yiwu.0579.com Xneox.com Zerocarts.com Wikidot.com Warpradio.com Topkam.ru Thumbnailworld.net Testron.ru Taskmanagementsoft.com Tagirov.org Storyme.app Searchdaimon.com Rentv.com Reefcentral.com Redcruise.com Puurconfituur.be Phpooey.com Openherd.com Myriad-online.com Muppetsauderghem.be Mientaynet.com Krimket.ro Jkes.tyc.edu.tw  Navigating the world of insurance can be complex and overwhelming, with numerous coverage options and policy details to consider. In this guide, we will provide you with valuable tips to help you choose the right insurance coverage for your specific needs. By following these tips, you can make informed decisions, secure adequate protection, and ensure peace of mind.

Assess Your Needs: Begin by assessing your insurance needs. Consider the risks you want to protect against, such as property damage, liability, health issues, or loss of income. Identify your priorities and evaluate the level of coverage required to adequately address these risks. Research Different Types of Coverage: Understand the different types of insurance coverage available, such as auto, home, renters, health, life, disability, and liability insurance. Research the purpose, features, and benefits of each type to determine which ones are relevant to your situation. This knowledge will guide you in selecting the right coverage. Evaluate Coverage Limits: Carefully evaluate the coverage limits offered by different insurance policies. Ensure that the limits align with your needs and potential risks. Consider factors such as property value, income level, liability exposure, or potential medical expenses to determine appropriate coverage limits. Understand Deductibles: Pay attention to the deductibles associated with insurance policies. A deductible is the amount you must pay out of pocket before the insurance coverage kicks in. Evaluate your financial situation and determine the deductible you can comfortably afford while considering the impact on your premiums. Compare Quotes: Obtain quotes from multiple insurance providers to compare coverage options and premiums. Ensure that you provide accurate information when requesting quotes to receive accurate estimates. Use online comparison tools or work with an independent insurance broker to simplify the comparison process. Consider Customer Service and Reputation: Evaluate the customer service reputation of insurance companies you are considering. Research their claims handling process, responsiveness, and overall customer satisfaction. Look for ratings and reviews from reputable sources to gain insights into their track record. Read and Understand Policy Terms: Thoroughly read and understand the terms and conditions of insurance policies before making a decision. Pay attention to exclusions, limitations, waiting periods, and any additional requirements. Seek clarification from the insurance provider or a professional if you have any questions or concerns. Seek Recommendations and Advice: Consult with friends, family members, or trusted advisors who have experience with insurance. They can provide insights and recommendations based on their own experiences. However, keep in mind that your insurance needs may differ, so consider their advice in conjunction with your own research. Seek Professional Guidance: Consider working with an independent insurance broker or agent who can provide expert guidance. These professionals have access to multiple insurance carriers and can help you navigate the options, explain policy details, and assist in finding the right coverage at the best possible price. Regularly Review and Update Coverage: Insurance needs change over time due to life events, changes in assets, or evolving risks. Regularly review your insurance coverage and update it as needed. Periodically reassess your needs, consult with professionals, and adjust your coverage to ensure it remains aligned with your current situation. Conclusion: Choosing the right insurance coverage requires careful assessment, research, and understanding of your needs. By assessing your needs, researching different types of coverage, evaluating coverage limits and deductibles, comparing quotes, considering customer service and reputation, reading and understanding policy terms, seeking recommendations and advice, seeking professional guidance, and regularly reviewing and updating your coverage, you can navigate the insurance maze with confidence. Remember, insurance is a crucial aspect of financial protection, so take the time to make informed decisions and secure the coverage that best suits your needs. Best Site Krimket.ro Puurconfituur.be Smokk.ru Krfan.ru Jepun.dixys.com Bavaria-munchen.com Morethanheartburn.com M.shopinanchorage.com Xneox.com Civicvoice.org.uk Rufox.ru Sat.issprops.com Nationalscholastic.org Searchdaimon.com Linkytools.com Archive.paulrucker.com Mosvedi.ru Notclosed.com Rea-awards.ru Nun.nu Bing.com Book.douban.com Bbs.pku.edu.cn Vi.paltalk.com Jkes.tyc.edu.tw  The claims process is a crucial aspect of insurance, as it allows policyholders to receive the benefits they are entitled to in times of need. Mastering the claims process can help ensure a smooth experience and a timely resolution. In this guide, we will provide you with essential tips to navigate the claims process effectively and maximize your chances of a successful insurance experience.

Understand Your Policy: Before filing a claim, thoroughly review your insurance policy to understand the coverage, exclusions, deductibles, and any specific requirements for filing a claim. Familiarize yourself with the terms and conditions to ensure you meet all necessary criteria. Document the Incident: When an incident occurs that may result in an insurance claim, document the details as accurately and comprehensively as possible. Take photos or videos of the damages or injuries, gather witness statements if applicable, and preserve any evidence related to the incident. Notify Your Insurance Company Promptly: Notify your insurance company promptly after the incident occurs. Most insurance policies require immediate reporting of incidents, and delaying the notification may result in claim denial. Provide all necessary information about the incident and follow the procedures outlined by your insurance company. Keep Detailed Records: Maintain detailed records of all communications related to your claim. Keep track of the date, time, and names of the individuals you speak with, including insurance company representatives, adjusters, or agents. Document the content of conversations, emails, and letters exchanged throughout the claims process. Cooperate with the Claims Adjuster: When a claims adjuster is assigned to your case, cooperate fully with them. Provide requested documentation promptly and answer their questions truthfully and accurately. Be responsive and accessible throughout the process to ensure a smooth evaluation of your claim. Follow Claim Submission Guidelines: Adhere to the claim submission guidelines provided by your insurance company. Ensure you include all required documentation, such as incident reports, police reports, medical records, repair estimates, or any other relevant information. Failing to provide necessary documentation may result in delays or denial of your claim. Review Estimates and Settlement Offers: Carefully review the estimates and settlement offers provided by your insurance company. Compare them to your own evaluations or independent assessments if necessary. If you believe the offer is insufficient, present additional evidence or seek professional advice to negotiate a fair resolution. Seek Professional Assistance if Needed: If you encounter challenges or disputes during the claims process, consider seeking professional assistance. Public adjusters or attorneys specializing in insurance claims can advocate on your behalf and ensure your rights are protected. They can provide guidance, navigate complex situations, and help you achieve a fair settlement. Maintain Patience and Persistence: The claims process can be complex and may require time and patience. Be prepared for potential delays and follow-up with your insurance company regularly to check the status of your claim. Maintain persistence in pursuing a fair resolution while being respectful and professional in your communications. Provide Feedback and Review: After your claim is resolved, provide feedback on your claims experience to your insurance company. Share your thoughts on the process, the responsiveness of their representatives, and the overall satisfaction with the outcome. Reviews and feedback can help insurance companies improve their services and benefit future policyholders. Conclusion: Mastering the claims process is essential for a smooth insurance experience. By understanding your policy, documenting the incident, notifying your insurance company promptly, keeping detailed records, cooperating with the claims adjuster, following claim submission guidelines, reviewing estimates and settlement offers, seeking professional assistance if needed, maintaining patience and persistence, and providing feedback, you can navigate the claims process effectively. Remember, staying informed, proactive, and organized will help ensure a successful insurance experience and a timely resolution of your claim. Network Archive.paulrucker.com Mosvedi.ru Notclosed.com Rea-awards.ru Nun.nu Bing.com Book.douban.com Bbs.pku.edu.cn Vi.paltalk.com Jkes.tyc.edu.tw Fr.paltalk.com Ezproxy.cityu.edu.hk Foro.infojardin.com Rs.rikkyo.ac.jp Aaoms.org Marillion.com Myriad-online.com Reefcentral.com Rexart.com Esvc000614.wic059u.server-web.com Blogranking.fc2.com Maultalk.com Warpradio.com Medknow.com Openherd.com  Life insurance is a crucial component of financial planning, providing protection and peace of mind for you and your loved ones. In this comprehensive overview, we will explore various life insurance options available to help you make informed decisions about your coverage. Understanding the different types of life insurance and their features will empower you to choose the right policy for your needs.

Term Life Insurance: Term life insurance offers coverage for a specific period, such as 10, 20, or 30 years. It provides a death benefit if the insured passes away during the term. Term life insurance is typically more affordable than other types of life insurance, making it suitable for those seeking temporary coverage, such as to protect a mortgage or support dependents during their working years. Whole Life Insurance: Whole life insurance is a permanent form of coverage that offers protection for the entire lifetime of the insured. It provides a death benefit to beneficiaries and accumulates a cash value component over time. Premiums for whole life insurance are generally higher than term life insurance, but the policy can build cash value that can be accessed during the insured's lifetime. Universal Life Insurance: Universal life insurance combines a death benefit with a flexible savings component. It allows policyholders to adjust their premium payments and death benefit amounts. Universal life insurance policies accrue cash value that can grow over time, and policyholders may have the option to access these funds or adjust the death benefit to meet changing needs. Variable Life Insurance: Variable life insurance offers a death benefit and a cash value component that is invested in various investment options. Policyholders have the potential to grow the cash value based on the performance of the investments. However, with variable life insurance, the cash value and death benefit are subject to market fluctuations and investment risk. Indexed Universal Life Insurance: Indexed universal life insurance provides a death benefit and a cash value component that is tied to the performance of a specified index, such as the S&P 500. Policyholders have the potential to earn interest based on the index's performance, while also having protection against downside market risk. Indexed universal life insurance offers flexibility in premium payments and death benefit amounts. Final Expense Insurance: Final expense insurance, also known as burial or funeral insurance, is designed to cover end-of-life expenses, such as funeral costs, medical bills, or outstanding debts. It typically provides a smaller death benefit compared to other life insurance policies and is intended to alleviate the financial burden on loved ones during a difficult time. Group Life Insurance: Group life insurance is typically offered through an employer or organization and provides coverage for a group of individuals. It offers convenience and affordability, often with no medical underwriting required. However, the coverage amount may be limited, and it may not be portable if you leave the group. Conclusion: Life insurance plays a vital role in protecting your loved ones and providing financial security. By understanding the various life insurance options, including term life insurance, whole life insurance, universal life insurance, variable life insurance, indexed universal life insurance, final expense insurance, and group life insurance, you can choose the policy that aligns with your needs, goals, and budget. It's important to evaluate your financial situation, consider your long-term objectives, and consult with a reputable insurance professional to determine the most suitable life insurance policy for you and your family. With the right life insurance coverage in place, you can ensure the financial well-being of your loved ones and have peace of mind for the future. Top Thing Thumbnailworld.net Shop-rank.com Dobrye-ruki.ru Findingreagan.com Gyo.tc Openroadbicycles.com Vstclub.com Extcheer.com Fondbtvrtkovic.hr Muppetsauderghem.be Dobrye-ruki.ru Nevinkaonline.ru Fudou-san.com Taskmanagementsoft.com Mientaynet.com Spacehike.com Ky.to l2base.su Ojkum.ru Profi.ua Troxellwebdesign.com Profi.ua Closingbell.co Bigmarty.com Chessburg.ru  Traditional insurance coverage may not always address the unique risks and needs of individuals or businesses with specialized requirements. That's where specialty insurance comes in. Specialty insurance provides tailored coverage for niche industries, unique assets, or specific risks that may not be adequately covered by standard policies. In this guide, we will explore the world of specialty insurance and its value in addressing unique needs.

Understanding Specialty Insurance: Specialty insurance refers to insurance coverage designed to address specific risks or industries that fall outside the scope of traditional insurance policies. It offers customized protection to individuals or businesses with unique needs, assets, or activities that require specialized coverage. Niche Industries: Specialty insurance caters to niche industries such as technology, entertainment, aviation, marine, sports, fine arts, and more. These industries often have specific risks and exposures that require specialized coverage tailored to their unique circumstances. Specialty insurance providers have expertise in these sectors and offer policies designed to address their specific needs. Unique Assets: Specialty insurance covers unique assets that may not be adequately protected by standard policies. This includes high-value properties, collectibles, jewelry, luxury vehicles, yachts, and other valuable items. Specialty insurance provides comprehensive coverage and higher limits to ensure these assets are fully protected. Non-Standard Risks: Specialty insurance also covers non-standard risks that are not typically covered by standard policies. Examples include cyber liability insurance, kidnap and ransom insurance, terrorism insurance, political risk insurance, and event cancellation insurance. These specialized policies address specific risks and provide financial protection for unique situations. Benefits of Specialty Insurance: Tailored Coverage: Specialty insurance policies are designed to address specific risks and provide comprehensive coverage that aligns with the needs of individuals or businesses in niche industries. Higher Coverage Limits: Specialty insurance offers higher coverage limits to adequately protect unique assets or mitigate non-standard risks. Expertise and Industry Knowledge: Specialty insurance providers have expertise and industry knowledge in their respective sectors, allowing them to better understand the risks involved and provide specialized guidance. Claims Handling: Specialty insurance providers often have dedicated claims teams with expertise in handling complex or specialized claims, ensuring a smoother claims process. Working with a Specialized Broker: When seeking specialty insurance coverage, it's advisable to work with a specialized insurance broker who understands the unique needs of your industry or asset. They can help assess your risks, identify appropriate coverage options, and connect you with reputable specialty insurance providers. A specialized broker can navigate the complexities of specialty insurance and tailor solutions that meet your specific requirements. Assessing Coverage and Exclusions: Just like any insurance policy, carefully review the terms, conditions, coverage limits, and exclusions of your specialty insurance policy. Understand what is covered and any specific conditions or requirements for coverage to ensure it aligns with your unique needs. Pay attention to any exclusions or limitations that may affect your coverage. Regular Review and Updates: As your circumstances change or your industry evolves, regularly review and update your specialty insurance coverage. This ensures that your policy remains relevant, accurately reflects your risks, and continues to provide adequate protection for your unique needs. Conclusion: Specialty insurance plays a crucial role in addressing the unique needs of individuals or businesses in niche industries, with unique assets, or facing non-standard risks. By understanding the value of specialty insurance, working with specialized brokers, and regularly reviewing and updating your coverage, you can ensure that your unique needs are adequately protected. Specialty insurance provides the peace of mind and tailored coverage necessary for navigating specialized industries and mitigating unique risks. Priority Boogiewoogie.com Centernorth.com Healthyeatingatschool.ca Marcellospizzapasta.com Brambraakman.com Luding.org Etarp.com Ittrade.cz Thumbnailworld.net Shop-rank.com Dobrye-ruki.ru Findingreagan.com Gyo.tc Openroadbicycles.com Vstclub.com Extcheer.com Fondbtvrtkovic.hr Muppetsauderghem.be Dobrye-ruki.ru Nevinkaonline.ru Fudou-san.com Taskmanagementsoft.com Mientaynet.com Spacehike.com Ky.to  In today's interconnected world, cyber threats pose a significant risk to individuals and businesses alike. Cyber insurance provides essential protection against the financial and reputational consequences of cyberattacks, data breaches, and other cyber incidents. In this guide, we will explore the importance of cyber insurance and provide insights on how to protect your digital assets in a connected world.

Understanding Cyber Insurance: Cyber insurance is designed to help individuals and businesses mitigate the financial impact of cyber incidents. It provides coverage for expenses related to data breaches, cyberattacks, identity theft, and other cyber threats. Cyber insurance policies can vary in coverage, so it's important to understand the specifics of the policy you choose. Assess Your Cyber Risk: Evaluate your cyber risk exposure by assessing your digital assets and potential vulnerabilities. Consider the sensitive data you possess, such as customer information or intellectual property, and identify potential weak points in your cybersecurity infrastructure. This assessment will help determine the appropriate level of cyber insurance coverage you need. Types of Cyber Insurance Coverage: Cyber insurance typically offers the following types of coverage: Data Breach Response: Covers expenses related to data breach notifications, credit monitoring for affected individuals, public relations efforts, and legal expenses. Cyber Extortion: Provides coverage for expenses associated with ransomware attacks or other forms of cyber extortion. Business Interruption: Covers losses resulting from network downtime, system failures, or cyber incidents that disrupt business operations. Cyber Liability: Protects against third-party claims resulting from data breaches, privacy violations, or other cyber-related incidents. Multimedia Liability: Covers claims arising from defamation, copyright infringement, or other intellectual property violations in online content. Understand Policy Exclusions and Limitations: Thoroughly review your cyber insurance policy to understand any exclusions and limitations. Some policies may not cover certain types of cyber incidents or may have specific requirements for coverage to be effective. It's crucial to understand these exclusions and limitations to avoid any surprises when filing a claim. Work with Cybersecurity Experts: When choosing cyber insurance coverage, consider partnering with cybersecurity experts or consultants. They can assess your cybersecurity measures, identify potential vulnerabilities, and provide recommendations to strengthen your defenses. Working with experts can help reduce your cyber risk and potentially lower insurance premiums. Develop a Cybersecurity Plan: Implement a comprehensive cybersecurity plan that includes strong security measures, employee training, regular software updates, and data backup protocols. A well-rounded cybersecurity strategy demonstrates your commitment to mitigating cyber risks and may positively impact your cyber insurance premiums. Maintain Incident Response Capabilities: Prepare for potential cyber incidents by establishing an incident response plan. This plan outlines the steps to take in the event of a breach or cyberattack, including communication protocols, containment measures, and coordination with relevant stakeholders. Demonstrating proactive incident response capabilities can be beneficial during the underwriting process for cyber insurance coverage. Regularly Review and Update Coverage: Cyber threats evolve rapidly, so it's important to regularly review and update your cyber insurance coverage. Assess changes in your digital assets, industry-specific risks, and emerging cyber threats to ensure your coverage remains adequate and up to date. Educate Employees: Invest in cybersecurity training for employees to raise awareness about cyber risks, phishing attacks, and other common threats. Educated employees are the first line of defense against cyber incidents and can play a significant role in mitigating risks. Complement Insurance with Risk Management: While cyber insurance provides financial protection, it's essential to complement it with robust risk management practices. Continuously assess and enhance your cybersecurity measures, monitor network activity for potential threats, and maintain backups of critical data. The combination of insurance and proactive risk management helps maximize your protection against cyber threats. Conclusion: Cyber insurance is a crucial component of protecting your digital assets in an interconnected world. By assessing your cyber risk, understanding coverage options, working with cybersecurity experts, implementing strong security measures, and regularly reviewing and updating your coverage, you can safeguard your digital assets and mitigate the financial impact of cyber incidents. Remember that cyber insurance is just one piece of the puzzle—complement it with a proactive risk management approach to enhance your overall cyber resilience. Top Site Thumbnailworld.net Shop-rank.com Dobrye-ruki.ru Findingreagan.com Gyo.tc Openroadbicycles.com Vstclub.com Extcheer.com Fondbtvrtkovic.hr Muppetsauderghem.be Dobrye-ruki.ru Nevinkaonline.ru Fudou-san.com Taskmanagementsoft.com Mientaynet.com Spacehike.com Ky.to l2base.su Ojkum.ru Profi.ua Troxellwebdesign.com Profi.ua Closingbell.co Bigmarty.com Chessburg.ru  Climate change has emerged as one of the most pressing challenges of our time, impacting ecosystems, economies, and communities worldwide. As the frequency and severity of extreme weather events increase, the insurance industry faces new and complex challenges in assessing risks, pricing policies, and providing adequate coverage. In this comprehensive article, we will explore the intersection of climate change and insurance, the evolving landscape of risk management, and the steps the insurance industry is taking to adapt to an uncertain future.

1. Climate Change and the Insurance Landscape Understanding Climate Change: Provide an overview of climate change, its causes, and the key ways it impacts the environment, including rising temperatures, increased precipitation, sea-level rise, and more frequent extreme weather events. Impact on Insurance: Discuss the implications of climate change on the insurance industry, including the increased frequency and severity of weather-related claims, the potential for uninsured losses, and the challenges of pricing policies and managing risks. 2. Assessing Climate Risks Risk Modeling and Analytics: Explain how the insurance industry utilizes sophisticated risk modeling and analytics to assess climate-related risks, including the probability of extreme weather events, property damage, and business interruption. Catastrophe Modeling: Discuss the role of catastrophe modeling in estimating potential losses from climate-related events, enabling insurers to anticipate and plan for large-scale disasters. 3. Adapting Insurance Products Parametric Insurance: Explore the concept of parametric insurance, which provides coverage based on predetermined parameters rather than traditional loss assessment, making it suitable for climate-related risks such as hurricanes, floods, or droughts. Index-Based Insurance: Discuss index-based insurance, where payouts are triggered by pre-defined indices related to climate or weather variables, providing coverage for agricultural losses, energy production, or tourism industries affected by climate-related events. 4. Sustainable Insurance Practices Environmental, Social, and Governance (ESG) Factors: Highlight the growing importance of ESG factors in insurance practices, including investments in environmentally sustainable projects, consideration of climate-related risks in underwriting, and promoting social and corporate responsibility. Climate Change Disclosures: Discuss the increasing demand for transparency and disclosure regarding insurers' climate change-related practices, including reporting on carbon footprints, climate risk management strategies, and sustainability initiatives. 5. Risk Mitigation and Adaptation Risk Mitigation Strategies: Explore the role of risk mitigation strategies, such as building codes, land-use planning, and investment in resilient infrastructure, in reducing climate-related risks and potential insurance losses. Climate Resilience and Adaptation: Discuss the importance of promoting climate resilience and adaptation measures, both at the individual and community levels, to reduce vulnerability and ensure long-term sustainability in the face of climate change. Conclusion Climate change poses significant challenges to the insurance industry, requiring proactive measures to assess risks, adapt insurance products, and promote sustainable practices. As the impacts of climate change continue to unfold, the insurance industry plays a crucial role in facilitating resilience and protecting individuals, businesses, and communities from climate-related risks. By embracing innovative solutions, implementing risk mitigation strategies, and integrating climate considerations into their operations, insurers can help society adapt to an uncertain future and foster a more sustainable and resilient world. Top Site Zooporn.blue Zinro.net Yiwu.0579.com Xneox.com Zerocarts.com Wikidot.com Warpradio.com Topkam.ru Thumbnailworld.net Testron.ru Taskmanagementsoft.com Tagirov.org Storyme.app Searchdaimon.com Rentv.com Reefcentral.com Redcruise.com Puurconfituur.be Phpooey.com Openherd.com Myriad-online.com Muppetsauderghem.be Mientaynet.com Krimket.ro Jkes.tyc.edu.tw  The gig economy has revolutionized the way people work, offering flexibility and independence to millions of freelancers and independent contractors. However, with this freedom comes the need for adequate insurance coverage to protect against potential risks and liabilities. In this comprehensive article, we will explore the importance of insurance for the gig economy, the specific coverage needs of freelancers and independent contractors, and the available insurance options to provide them with financial protection and peace of mind.

1. Understanding the Gig Economy and Insurance Needs Exploring the Gig Economy: Define the gig economy and its growing influence on the modern workforce, highlighting the diverse range of professions and services that fall under this category. Unique Insurance Considerations: Discuss the unique insurance considerations for gig economy workers, including the need for liability coverage, property protection, income protection, and healthcare coverage. 2. Liability Coverage for Gig Workers General Liability Insurance: Explain the importance of general liability insurance for gig workers, which protects against third-party claims for bodily injury, property damage, or advertising injuries that may arise while providing services. Professional Liability Insurance: Discuss the significance of professional liability insurance, also known as errors and omissions insurance, for gig workers who offer professional services or advice, protecting against claims of negligence, errors, or omissions. Cyber Liability Insurance: Highlight the growing need for cyber liability insurance, especially for gig workers who handle sensitive client data or rely heavily on technology for their work, providing protection against data breaches, cyber attacks, and potential legal consequences. 3. Property Protection for Gig Workers Business Property Insurance: Explain the importance of business property insurance for gig workers who own or rent equipment, tools, or office space required to perform their services, providing coverage against damage, theft, or loss. Commercial Auto Insurance: Discuss the need for commercial auto insurance for gig workers who use their vehicles for business purposes, ensuring coverage in case of accidents, property damage, or injuries to third parties. 4. Income Protection for Gig Workers Disability Insurance: Highlight the significance of disability insurance for gig workers, providing income replacement if they are unable to work due to illness, injury, or disability. Unemployment Insurance: Discuss the availability of unemployment insurance for gig workers in certain jurisdictions, providing a safety net during periods of unemployment or when contracts end. 5. Healthcare Coverage for Gig Workers Health Insurance Options: Explore different healthcare coverage options available to gig workers, including individual health insurance plans, health savings accounts (HSAs), or participation in healthcare marketplaces or professional associations. Telemedicine and Health Tech: Discuss the emerging trends of telemedicine and health tech that offer convenient and accessible healthcare solutions for gig workers, enabling them to access medical advice and consultations remotely. Conclusion The gig economy offers tremendous opportunities for freelancers and independent contractors to create their own path and pursue their passions. However, with these opportunities come unique risks and challenges. Securing appropriate insurance coverage is crucial to protect against potential liabilities, property damage, income loss, and healthcare expenses. By understanding the specific insurance needs of gig workers and exploring the available coverage options, freelancers and independent contractors can ensure they have the necessary financial protection to thrive in the gig economy. Investing in insurance not only safeguards their business and personal assets but also provides peace of mind, allowing them to focus on their work and seize the opportunities that the gig economy presents. Recommended Showhorsegallery.com Testron.ru Zinro.net Aurki.com Halgatewood.com Dantzaedit.liquidmaps.org Halgatewood.com Sindbadbookmarks.com Landmarks-stl.org Skateroom.com Fastzone.org Whois.hostsir.com Dogjudge.com Domnabali.com Fastzone.org Beton.ru Oldcardboard.com Boogiewoogie.com Centernorth.com Healthyeatingatschool.ca Marcellospizzapasta.com Brambraakman.com Luding.org Etarp.com Ittrade.cz  Hobbies and recreational activities bring joy, fulfillment, and excitement to our lives. Whether you enjoy sports, collectibles, arts and crafts, or outdoor adventures, it's essential to protect your investments and passion with appropriate insurance coverage. In this comprehensive article, we will explore the importance of insuring your hobbies and recreational activities, the types of coverage available, and how it can safeguard your dreams and provide peace of mind.

1. Understanding the Risks Risks Associated with Hobbies: Discuss the potential risks and liabilities that can arise from participating in hobbies and recreational activities, such as injuries, property damage, theft, or loss. Unique Coverage Needs: Highlight how hobbies often involve specialized equipment, valuable collections, or unique liability considerations, necessitating specialized insurance coverage to protect against potential losses. 2. Types of Insurance Coverage Personal Liability Insurance: Explain the importance of personal liability coverage, which protects you if you accidentally cause injury to others or damage their property while engaging in your hobby or recreational activity. Property Insurance: Discuss the need for property insurance to protect valuable equipment, collectibles, or supplies associated with your hobbies, such as cameras, musical instruments, sports gear, or art materials. Specialty Insurance: Explore specialized insurance policies tailored to specific hobbies or activities, such as collectibles insurance, fine arts insurance, boat or watercraft insurance, or event insurance for organizing hobby-related gatherings or exhibitions. 3. Evaluating Coverage Options Assessing Coverage Needs: Provide guidance on assessing your unique coverage needs based on the nature of your hobby or recreational activity, the value of your assets, and the potential risks involved. Policy Limits and Deductibles: Discuss the importance of understanding policy limits, deductibles, and coverage exclusions, ensuring that your insurance policy adequately covers the value of your assets and potential liabilities. Researching Insurance Providers: Encourage individuals to research and compare insurance providers, considering factors such as reputation, coverage options, customer service, and pricing to find the best fit for their specific hobby or recreational activity. 4. Tips for Insuring Your Hobbies Proper Documentation: Emphasize the importance of keeping detailed records, including receipts, appraisals, and photographs of valuable items associated with your hobby, to streamline the claims process and substantiate the value of your assets. Safety Measures: Highlight the significance of practicing safety measures and adhering to any licensing or certification requirements associated with your hobby, as it can potentially influence your insurance coverage and premiums. Regular Policy Reviews: Encourage individuals to regularly review and update their insurance policies to ensure they reflect any changes in their hobbies, the value of their assets, or their liability exposure. Conclusion Your hobbies and recreational activities are an expression of your passion and personal fulfillment. Insuring your dreams with appropriate coverage helps protect your investments, assets, and financial well-being. By understanding the risks, evaluating coverage options, and taking proactive steps to insure your hobbies, you can enjoy your pursuits with peace of mind, knowing that you are prepared for unexpected events. Whether you collect rare items, engage in adventurous sports, or pursue artistic endeavors, insurance coverage tailored to your hobbies can safeguard your dreams and provide the necessary support when you need it most. New Service Chla.ca Studioad.ru Infoholix.net Lastapasdelola.com 18to19.com Davidpawson.org Centroarts.com Kassirs.ru Yiwu.0579.com Zooporn.blue Infohelp.com Unicom.ru Good-surf.ru Lp-inside.ru Pyi.co.nz Good-surf.ru Lostnationarchery.com Orbiz.by Start365.info Vodotehna.hr Storyme.app Tagirov.org Onekingdom.us Biyougeka.esthetic-esthe.com M.mobilegempak.com  Throughout our lives, we face various risks and uncertainties that can impact our financial well-being and that of our loved ones. Insurance provides a crucial safety net, offering protection against unforeseen events and providing peace of mind. However, the insurance coverage needed can vary depending on the stage of life we are in. In this comprehensive article, we will explore the different insurance needs at each stage of life, from birth to retirement, helping individuals make informed decisions about the types and levels of coverage required for comprehensive protection.

1. Insurance Needs for Children and Young Adults Health Insurance: Discuss the importance of health insurance for children and young adults, covering medical expenses, preventive care, and potential illnesses or accidents. Life Insurance for Parents: Address the need for life insurance coverage for parents, ensuring financial security for their children in case of the parents' untimely death. 2. Insurance Needs for Young Professionals and Families Life Insurance: Explain the significance of life insurance for young professionals and families, providing income replacement, debt coverage, and financial protection for dependents in the event of the policyholder's death. Disability Insurance: Discuss the importance of disability insurance, which replaces a portion of income if the policyholder becomes disabled and unable to work. Health Insurance: Emphasize the need for comprehensive health insurance coverage for individuals and families, protecting against medical expenses and ensuring access to quality healthcare. Homeowners/Renters Insurance: Highlight the importance of homeowners or renters insurance, covering property damage, liability, and providing temporary living expenses in case of unforeseen events such as fire, theft, or natural disasters. 3. Insurance Needs for Mid-Career Professionals Life Insurance: Discuss the continued need for life insurance to protect dependents and cover financial obligations such as mortgages, education expenses, and outstanding debts. Disability Insurance: Reiterate the importance of disability insurance, safeguarding income in case of a disability that prevents the policyholder from working. Long-Term Care Insurance: Address the need for long-term care insurance, which covers the costs of assisted living, nursing home care, or in-home care services in later years. 4. Insurance Needs for Pre-Retirement and Retirement Life Insurance: Explain how life insurance needs may change during the pre-retirement and retirement phase, focusing on legacy planning, estate considerations, and final expenses. Long-Term Care Insurance: Reiterate the importance of long-term care insurance to cover potential long-term care needs, protecting retirement savings from the high costs of care. Medicare Supplement Insurance: Discuss the importance of Medicare supplement insurance to fill the gaps in Medicare coverage and provide additional benefits for healthcare needs. Travel Insurance: Highlight the significance of travel insurance for retirees, providing coverage for medical emergencies, trip cancellation, or lost baggage during domestic or international travel. 5. Regular Policy Reviews and Updates Emphasize the importance of regular policy reviews and updates at each stage of life to ensure that coverage aligns with changing circumstances, needs, and goals. Conclusion Insurance is a vital component of financial planning at every stage of life, providing protection and peace of mind for individuals and their families. By understanding the insurance needs at each stage, individuals can make informed decisions about the types and levels of coverage required for comprehensive protection. Regular policy reviews and updates ensure that coverage remains relevant and effective as circumstances change. Ultimately, having appropriate insurance coverage throughout life safeguards against financial uncertainties, allowing individuals to focus on enjoying each stage with confidence and security. Top Thing Chla.ca Studioad.ru Infoholix.net Lastapasdelola.com 18to19.com Davidpawson.org Centroarts.com Kassirs.ru Yiwu.0579.com Zooporn.blue Infohelp.com Unicom.ru Good-surf.ru Lp-inside.ru Pyi.co.nz Good-surf.ru Lostnationarchery.com Orbiz.by Start365.info Vodotehna.hr Storyme.app Tagirov.org Onekingdom.us Biyougeka.esthetic-esthe.com M.mobilegempak.com  Insurance policies are vital financial contracts that provide protection and peace of mind in various areas of life. However, understanding the terms and conditions outlined in insurance policies can often be challenging due to the extensive amount of information and legal jargon involved. In this comprehensive article, we will delve into the intricacies of insurance policy terms and conditions, explaining their importance, common components, and offering tips to help policyholders navigate and comprehend the fine print of their insurance coverage.

1. The Importance of Reading the Fine Print Contractual Obligations: Discuss the significance of insurance policies as legally binding contracts, emphasizing the need for policyholders to understand their rights, responsibilities, and the scope of coverage. Coverage Limitations: Explain how the fine print clarifies the limitations and exclusions of the insurance coverage, ensuring policyholders have a realistic understanding of what is and isn't covered. 2. Common Components of Insurance Policy Terms and Conditions Insuring Agreement: Explain the insuring agreement, which outlines the scope of coverage provided by the insurance policy and the specific risks or events that trigger coverage. Definitions: Discuss the importance of definitions within insurance policies, as they clarify the meanings of key terms and terms unique to the policy. Coverage Conditions: Address the coverage conditions, which outline the requirements and obligations that policyholders must meet to maintain coverage, such as timely premium payments and accurate reporting of information. Exclusions and Limitations: Highlight the exclusions and limitations section, which specifies the circumstances, events, or risks that the insurance policy does not cover or places restrictions upon. Deductibles and Co-Payments: Explain how deductibles and co-payments work, outlining the portion of a claim that the policyholder must pay out of pocket before the insurance coverage kicks in. Claims Process: Discuss the terms and conditions related to the claims process, including the notification requirements, documentation needed, and the timeframe for filing a claim. 3. Tips for Understanding the Fine Print Read Carefully: Encourage policyholders to read the insurance policy carefully, paying attention to each section and referring to the definitions to ensure a clear understanding. Seek Clarification: Suggest reaching out to the insurance provider or agent to seek clarification on any unclear terms, conditions, or coverage aspects. Ask Questions: Recommend policyholders to ask questions about any areas of the policy they don't understand or require further explanation. Document Communication: Advise policyholders to document all communication with the insurance provider or agent, including dates, times, and names of individuals spoken to, to keep a record of important discussions. Seek Professional Help: Suggest consulting with an insurance professional or legal advisor if the policyholder encounters complex policy language or requires further assistance in understanding the terms and conditions. 4. Reviewing and Updating Coverage Regular Policy Review: Emphasize the importance of reviewing the insurance policy periodically, especially during major life changes or policy renewal, to ensure that the coverage still aligns with the policyholder's needs. Policy Updates: Highlight the need to update the insurance policy when changes occur in the insured property, assets, or circumstances that may impact coverage requirements. Conclusion Understanding the terms and conditions of an insurance policy is essential for policyholders to maximize the benefits of their coverage and avoid any surprises or misunderstandings during the claims process. By carefully reading, seeking clarification, and asking questions about the fine print, policyholders can gain a clear understanding of their rights, responsibilities, and the limitations of their insurance coverage. Regular policy reviews and updates further ensure that the coverage remains relevant and effective over time. By demystifying the fine print, policyholders can make informed decisions and confidently navigate the intricacies of their insurance policies. New Part Start365.info Spacehike.com Skateroom.com Showhorsegallery.com Shop-rank.com Sha.org.sg Services.nfpa.org Sat.issprops.com Rs.rikkyo.ac.jp Rea-awards.ru Pyi.co.nz Projectbee.com Profi.ua Profi.ua Orbiz.by Openroadbicycles.com Ojkum.ru Nevinkaonline.ru Mosvedi.ru Marillion.com Marcellospizzapasta.com M.shopinanchorage.com M.mobilegempak.com Luding.org Lp-inside.ru  Motorcycles and two-wheelers offer a thrilling and liberating mode of transportation. However, as a rider, it's essential to prioritize safety and protect yourself against potential risks on the road. Motorcycle insurance plays a crucial role in providing financial protection, peace of mind, and legal compliance for riders. In this comprehensive article, we will explore the importance of motorcycle insurance, its key features, coverage options, and tips for securing the right insurance to ride with peace of mind.

1. The Importance of Motorcycle Insurance Financial Protection: Discuss the significance of motorcycle insurance in providing financial coverage for damages to your motorcycle, medical expenses in case of an accident, and liability protection against third-party claims. Legal Compliance: Address the legal requirements of motorcycle insurance, emphasizing the need to meet the minimum insurance requirements set by local authorities. 2. Motorcycle Insurance Coverage Options Liability Insurance: Explain how liability insurance covers bodily injury and property damage liability, providing financial protection if you are at fault in an accident that causes harm to others or damages their property. Collision Coverage: Discuss collision coverage, which covers the cost of repairing or replacing your motorcycle in the event of an accident, regardless of fault. Comprehensive Coverage: Highlight comprehensive coverage, which provides protection against non-collision incidents such as theft, vandalism, natural disasters, or damage caused by animals. Medical Payments Coverage: Address the importance of medical payments coverage, which covers medical expenses for injuries sustained in a motorcycle accident, regardless of fault. Uninsured/Underinsured Motorist Coverage: Explain the significance of uninsured/underinsured motorist coverage, which protects you if you are involved in an accident with a driver who lacks sufficient insurance coverage. 3. Factors to Consider When Choosing Motorcycle Insurance Riding Habits and Usage: Discuss how your riding habits, including frequency, distance, and type of riding, can influence the level of coverage and premiums. Motorcycle Value: Highlight the impact of the motorcycle's value, age, make, and model on insurance premiums, as more expensive or high-performance motorcycles may require higher coverage. Deductibles and Coverage Limits: Address the importance of selecting appropriate deductibles and coverage limits that align with your budget and potential financial risks. Discounts and Bundling Options: Explain the availability of discounts for factors such as safety training courses, multiple policies with the same insurer (e.g., bundling with auto insurance), and anti-theft devices. 4. Additional Considerations Gear and Accessories Coverage: Discuss the availability of coverage for riding gear, accessories, and modifications to your motorcycle, ensuring protection for your investments. Roadside Assistance: Highlight the importance of considering roadside assistance coverage, which can provide assistance in case of breakdowns, flat tires, or other emergencies while riding. Policy Renewal and Review: Emphasize the significance of regularly reviewing your policy, considering any changes in your riding habits, motorcycle value, or coverage needs. 5. Safety and Risk Management Training and Skill Development: Encourage riders to participate in motorcycle safety training courses to enhance riding skills and reduce the risk of accidents. Defensive Riding Practices: Discuss the importance of adopting defensive riding techniques, maintaining awareness of road conditions, and following traffic rules to mitigate risks. Proper Maintenance: Highlight the significance of regular motorcycle maintenance, including tire checks, brake inspections, and fluid changes, to ensure optimal safety and performance. Conclusion Motorcycle insurance is essential for riders to protect themselves, their motorcycles, and their financial well-being. By understanding the importance of motorcycle insurance, evaluating coverage options, considering key factors, and prioritizing safety, riders can confidently hit the road knowing they are protected in the event of an accident or unforeseen circumstances. Riding with peace of mind allows riders to fully enjoy the freedom and exhilaration that motorcycles and two-wheelers offer while ensuring they are financially protected and compliant with legal requirements. Priority Marillion.com Myriad-online.com Reefcentral.com Rexart.com Esvc000614.wic059u.server-web.com Blogranking.fc2.com Maultalk.com Warpradio.com Medknow.com Openherd.com Pornreviews.pinkworld.com Redcruise.com Morhipo.com Bigcosmic.com Druglibrary.net Zerocarts.com Sha.org.sg Vn.com.ua Rentv.com Superfos.com Torahlab.org Clevelandbay.com Fcterc.gov.ng Silverdart.co.uk Freshcannedfrozen.ca  Auto accidents are unfortunate events that can cause significant damage to vehicles and result in injuries to drivers, passengers, and pedestrians. To protect against the financial implications of such incidents, auto insurance plays a crucial role in providing coverage for vehicle damage and medical expenses. In this comprehensive article, we will explore the world of auto insurance, specifically focusing on coverage for accidents and vehicle damage. By understanding the different types of coverage, the claims process, and important considerations, readers will be better equipped to navigate the road to recovery after an auto accident.

1. The Importance of Auto Insurance Financial Protection: Emphasize the significance of auto insurance in providing financial protection against potential liabilities and property damage resulting from accidents. Legal Requirements: Discuss the legal requirements for auto insurance, including mandatory liability coverage in many jurisdictions. 2. Understanding Auto Insurance Coverage Liability Coverage: Explain liability coverage, which protects the policyholder against claims made by others for property damage or injuries resulting from an accident for which the policyholder is responsible. Collision Coverage: Discuss collision coverage, which provides compensation for damage to the policyholder's vehicle resulting from a collision with another vehicle or object. Comprehensive Coverage: Address comprehensive coverage, which protects against non-collision-related damages, such as theft, vandalism, fire, natural disasters, and falling objects. Personal Injury Protection (PIP)/Medical Payments Coverage: Explain PIP or medical payments coverage, which covers medical expenses for the policyholder and passengers injured in an accident, regardless of fault. 3. Factors Affecting Auto Insurance Premiums Driving History: Discuss how factors like past accidents, traffic violations, and claims history can impact auto insurance premiums. Vehicle Type: Explain how the make, model, age, and value of the vehicle can affect insurance premiums. Coverage Limits and Deductibles: Discuss how selecting higher coverage limits or lower deductibles can impact premiums. Location and Usage: Address how the location where the vehicle is parked or driven, as well as the frequency of use, can affect insurance premiums. 4. Filing an Auto Insurance Claim Contacting the Insurance Company: Outline the steps to follow after an accident, including notifying the insurance company as soon as possible. Collecting Information: Discuss the importance of gathering necessary information, such as the details of the accident, contact information of involved parties, and any available photographic evidence. Documenting Damages: Explain the significance of documenting the vehicle damage, including taking photographs and obtaining repair estimates. Medical Reports and Documentation: Discuss the importance of obtaining medical reports, documenting injuries, and retaining medical bills and receipts for reimbursement. Working with Claims Adjusters: Highlight the role of claims adjusters in assessing the damage, determining fault, and guiding policyholders through the claims process. 5. Rental Car Coverage and Towing Services Rental Car Coverage: Explain the availability of rental car coverage as part of an auto insurance policy, which provides reimbursement for the cost of a rental vehicle during repairs. Towing and Roadside Assistance: Discuss the inclusion of towing services and roadside assistance in some auto insurance policies, providing support for mechanical breakdowns and emergencies. 6. Considerations for Vehicle Repairs Preferred Repair Shops: Discuss the option of using preferred repair shops recommended by the insurance company, as well as the freedom to choose an alternative repair facility. Parts and Labor Coverage: Address the coverage for original manufacturer parts and labor costs associated with vehicle repairs. 7. Claims Disputes and Resolving Issues Appealing Claim Decisions: Explain the process of appealing claim decisions if there are disputes over coverage, liability, or settlement amounts. Mediation and Arbitration: Discuss the potential involvement of mediation or arbitration to resolve claim disputes outside of court. Conclusion Auto insurance plays a crucial role in providing financial protection and peace of mind for drivers in the event of accidents and vehicle damage. By understanding the various types of coverage, factors influencing premiums, the claims process, and considerations for vehicle repairs, individuals can navigate the road to recovery with confidence. Auto insurance ensures that policyholders have the necessary support and financial resources to repair their vehicles, cover medical expenses, and move forward after an auto accident. Top Thing Marillion.com Myriad-online.com Reefcentral.com Rexart.com Esvc000614.wic059u.server-web.com Blogranking.fc2.com Maultalk.com Warpradio.com Medknow.com Openherd.com Pornreviews.pinkworld.com Redcruise.com Morhipo.com Bigcosmic.com Druglibrary.net Zerocarts.com Sha.org.sg Vn.com.ua Rentv.com Superfos.com Torahlab.org Clevelandbay.com Fcterc.gov.ng Silverdart.co.uk Freshcannedfrozen.ca  Health insurance is an essential component of modern healthcare, providing individuals and families with access to necessary medical services while mitigating the financial burden of healthcare expenses. However, navigating the complex world of health insurance can be challenging, with various coverage options, terms, and regulations to understand. In this comprehensive article, we will decode health insurance, helping readers gain a deeper understanding of the intricacies of medical coverage. By exploring the key concepts, types of plans, and important considerations, individuals can make informed decisions regarding their health insurance coverage and maximize its benefits.

1. The Importance of Health Insurance Financial Protection: Highlight the significance of health insurance in protecting against the high costs of medical treatments, hospital stays, surgeries, and prescription medications. Access to Quality Healthcare: Discuss how health insurance grants individuals access to a network of healthcare providers, ensuring timely and comprehensive medical care. 2. Understanding Health Insurance Terminology Premiums: Explain the concept of premiums, the regular payments individuals make to maintain their health insurance coverage. Deductibles: Discuss deductibles, the amount individuals must pay out of pocket before the insurance coverage kicks in. Co-payments and Co-insurance: Explain the difference between co-payments (fixed amounts individuals pay for specific services) and co-insurance (the percentage of costs individuals share with the insurance company after meeting the deductible). Out-of-Pocket Maximums: Discuss the out-of-pocket maximum, the limit on the total amount individuals are required to pay in a given policy period. 3. Types of Health Insurance Plans Health Maintenance Organization (HMO): Explain the features of HMO plans, including primary care physicians, referral requirements, and network restrictions. Preferred Provider Organization (PPO): Discuss the characteristics of PPO plans, such as the flexibility to see specialists without referrals and the option to choose both in-network and out-of-network providers. Point of Service (POS): Describe POS plans, which combine features of HMO and PPO plans, allowing individuals to choose between primary care physicians and the freedom to see out-of-network specialists. High Deductible Health Plans (HDHP): Address the features of HDHPs, including higher deductibles and lower premiums, often accompanied by Health Savings Accounts (HSAs) or Health Reimbursement Arrangements (HRAs) to help individuals manage healthcare costs. 4. Coverage Considerations and Services Preventive Care: Highlight the importance of preventive care services, such as vaccinations, screenings, and wellness visits, which are often covered at no cost under health insurance plans. Hospitalization and Emergency Care: Discuss coverage for hospital stays, emergency room visits, and urgent care services, including the role of preauthorization and network considerations. Prescription Medications: Address coverage for prescription drugs, including formularies, tiers, and potential cost-saving strategies like generic substitution and mail-order pharmacies. Specialized Care: Explore coverage for specialized care, such as mental health services, rehabilitation, maternity care, and chronic disease management. 5. Network Considerations and Provider Choice In-Network vs. Out-of-Network Providers: Explain the differences between in-network and out-of-network providers, highlighting the importance of staying within the network to maximize coverage and minimize out-of-pocket expenses. Provider Directories: Discuss the significance of reviewing provider directories to ensure access to preferred healthcare professionals, specialists, hospitals, and other healthcare facilities. 6. Enrollment Periods and Open Enrollment Initial Enrollment Period: Explain the initial enrollment period for health insurance, typically associated with specific life events or eligibility criteria. Annual Open Enrollment: Discuss the annual open enrollment period when individuals can enroll, switch, or update their health insurance coverage. 7. Patient Rights and Advocacy Health Insurance Portability and Accountability Act (HIPAA): Address patient rights and privacy protections under HIPAA, ensuring the confidentiality and security of personal health information. Appeals and Grievances: Explain the process for filing appeals or grievances with insurance companies if disputes arise regarding coverage denials or payment issues. Conclusion Understanding the complexities of health insurance is vital for individuals and families to make informed decisions about their coverage, access quality healthcare, and protect themselves financially. By decoding health insurance terminology, exploring different plan options, considering coverage and services, and understanding network considerations, individuals can navigate the world of health insurance with confidence. Equipped with this knowledge, individuals can advocate for their healthcare needs, maximize the benefits of their health insurance, and prioritize their well-being in an increasingly complex healthcare landscape. New Part Nyl0ns.com Hudsonvalleytraveler.com Urcountry.ru Krimket.ro Puurconfituur.be Smokk.ru Krfan.ru Jepun.dixys.com Bavaria-munchen.com Morethanheartburn.com M.shopinanchorage.com Xneox.com Civicvoice.org.uk Rufox.ru Sat.issprops.com Nationalscholastic.org Searchdaimon.com Linkytools.com Archive.paulrucker.com Mosvedi.ru Notclosed.com Rea-awards.ru Nun.nu Bing.com Book.douban.com  Life is filled with unexpected events that can disrupt our plans, challenge our financial security, and create emotional distress. To navigate these uncertainties, insurance serves as a crucial tool for protecting ourselves, our loved ones, and our assets. In this comprehensive article, we will explore the importance of planning for life's unexpected events through insurance. By understanding the types of coverage available and implementing effective strategies, individuals and families can ensure greater financial stability, peace of mind, and resilience in the face of unforeseen circumstances.