How Term Life Insurance Works

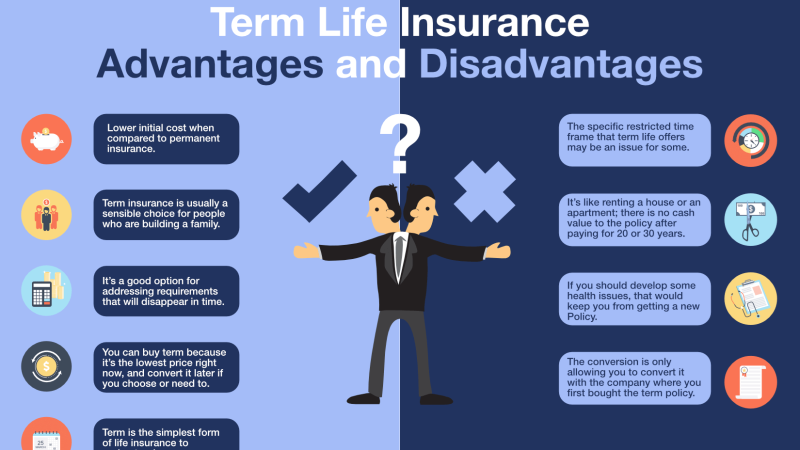

Term life insurance was one of the first forms of life insurance available. It provides life insurance at a fixed rate for a certain time period or term. After the time period or term expires, then the coverage at the former premium is not guaranteed and the insured must either go without life insurance, or get another policy with different payments and conditions if the same type of policy cannot be obtained. If an insured party passes away while they are actively making payments on their term life policy, then the money from the policy would go to the beneficiary they named in the policy. Term life insurance is usually the cheapest way to go when buying life insurance. Term life only insures the person for as long as the premiums are made for the predetermined amount of time. In contrast, a person who buys permanent life insurance is guaranteed coverage for the whole length of their life. Beware Of A Lapse In Payment Term insurance works like car or home insurance. If the premiums are paid and up-to-date, then the policy is active. If the insured lapses on payments or is late then there is a risk of losing coverage. Even if one monthly premium is missed there is the risk of not being paid the death benefit. The premium rate is determined on several factors, namely how likely it is that the insurance company will have to pay out on the policy within the life of the insurance policy. If you have a pre-existing condition or work in a high-risk field, your premiums may be higher than someone who is healthy with a sedentary job. Term life insurance is not recommended if you are looking for long-term coverage. Some people will purchase term life insurance before they leave the country for a trip or if they plan on embarking on a risky adventure such as parachuting out of an airplane or engaging in a life-threatening activity. Term life policies have gained popularity in this day of extreme sports.

1 Comment

Universal Life Insurance Relies On Investments

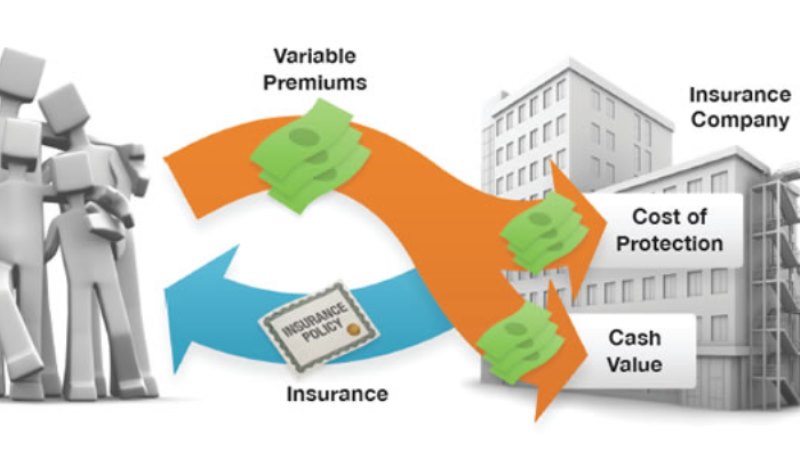

Universal life insurance policies require you to make monthly payments towards the insurance. This is true of any life insurance policy. However, universal life insurance is different in that the life insurance company invests the money they receive in bonds, money markets and even mortgages. In return for the freedom with the money, they promise you will earn interest on the money you pay. If their investments pay off, the amount you’ll earn in interest can be quite high. If they fail, you’ll be earning a minimal amount. How Monthly Premiums Are Calculated Your monthly premium factors in a few things. Because your money is gaining interest, the insurance company will reduce the interest from your monthly payment. This changes the amount you owe from month to month. Administrative fees against the account will also affect your payment. Setting Up A Universal Life Insurance Policy When you set up a universal life policy, you have two options: A or B. The choice you make affects the money your beneficiary receives at death. With Option A, your interest accrues over time. When you die, the company subtracts the amount of interest from the face value of the life insurance policy and sends the difference to your beneficiary. A policy with Option A costs you less in premiums. Option B involves adding the amount you’ve earned in interest over the years to the face value of your life insurance policy. If your life insurance policy has performed well, the amount your beneficiary can be substantially more than the face value. With either option, the premium you pay usually includes a “no-lapse guarantee.” This means that your premium amount will never change unless you pay your bill late or skip a payment. If that happens, you may need to re-enroll. Otherwise, you keep the same monthly premium until your 100th birthday. Pros And Cons To Universal Life Insurance Policies The biggest benefit to a universal life insurance policy is that the premiums are generally affordable. However, it also lulls people into paying the minimal amount and this may backfire over time. The amount in your www.impianking4d.com account will not grow enough to make your interest worthwhile. With some companies, if you do not increase the amount you pay, your account may lapse. This is especially true if the insurance company’s investments do not pay out as high as they did the month before. If your interest earnings decrease you will need to increase your monthly payment to cover the difference.  Development Of Whole Life Insurance

Whole life insurance was developed to ease the turmoil over term life policies. Consumers were upset that they could potentially be making monthly premiums on life insurance for twenty to thirty years. With a whole life policy, higher premiums are paid over a predetermined amount of time for a certain policy amount. Even if the insured only paid the premiums for ten years, the coverage would last until their death even if they died after they completed making the monthly premiums. Participants in a whole life policy also have the option of cashing in the policy after the policy matured, between 94 and 100 years old. There Are Several Types There are several different types of whole life insurance; single-premium, non-participating, economic, limited pay, participating, indeterminate whole life and a newer form, interest-sensitive whole life. The types of policies offered vary by insurance company and the state the policy is purchased in. In a single-premium policy the total premium is paid up front. In a non-participating policy all values pertaining to the policy, including death benefits and cash value, are determined when the policy is purchased and cannot be changed after the policy has been purchased. In a participating policy the insurance company shares the profit made from other policies with the participating policyholder in the form of overcharges on premiums and refunds. An economic policy is a mix of term life and participating insurance. In this policy the extra money is used to purchase additional life insurance resulting in a higher pay out after death and a larger cash value. A limited pay policy is like a participating policy but the premiums are paid out for a limited number of years instead of the life of the insured. Indeterminate whole life insurance is similar to a non-participating policy but the premiums may vary from year to year. The newest form of life insurance, interest-sensitive insurance, is a mix of universal life insurance and whole life insurance. Certain causes of death are covered while others are not. Special Circumstances Typically in all forms of whole life insurance, the policy premiums must be paid by the insured and not by another party unless there are special circumstances. There has been a rash of deaths for insurance policies and the insurance companies are starting to restrict who can pay on the policy.  There are many types of life insurance. The two most familiar terms are whole life and term life, which are both self-explanatory in meaning. The whole life insurance policy covers an individual for his whole life, whereas the term life insurance policy covers an individual for a certain term of his life.

Pro life insurance is a term used within insurance companies that will promote the need and use of life insurance. Life insurance is important to everyone. If you are married, life insurance is important both to you and your spouse. If you are married and have children, life insurance becomes even more important for you, your spouse and your family members. Most life insurance companies will allow for most of your “purchase” options of life insurance to be completed online. You can requests quotes, ask questions and answer the questionnaire online or on the telephone. Some life insurance can even be finalized online or on the phone because certain policies can be bought without the requirement of any medical records and/or exams. Benefits Of Life Insurance Once you have secured a life insurance policy at www.dominoz88.com, there is a peace of mind that comes with knowing if something were to happen to you, your spouse and/or your family will be provided for the future. Depending on the type of life insurance you purchase, your life insurance benefit can provide the funding of college, estates and even be saved for any future grandchildren to have their needs provided for. Most life insurance policies can be beneficial to you while you are still alive. Depending on the type of life insurance you purchase, you can invest the funds with a monthly, semi-monthly or yearly benefit to be paid to you through interest and/or dividend checks. This type of life insurance provides supplemental income to you, your spouse and/or your family. So, every individual can benefit for being covered under a life insurance plan.  The Necessity Of Life Insurance

According to a funeral director in New Hartford, Connecticut, the average price of a funeral in 2009 is $7,000. If you die, could your family afford to have you buried? For most people the answer is no, and this is only the beginning. Once you die, your spouse or significant other and children face life without your income. They become responsible for your debts. Unless you have huge bank accounts, most families face bankruptcy when left with mounting debts and reduced income. Social security may offer survivor benefits, but the amount varies and may not be enough. This explains the importance of life insurance. The Facts About Life Insurance When you purchase life insurance policies, companies group similarly aged people together and then calculate the chances of people in that group dying against the money they would have to pay out. They use this information to come up with your monthly, quarterly or yearly premiums. If you do pass away, the company must pay the face value of the policy to the beneficiary listed on the application. This money is not taxable and helps keep surviving family members or loved ones from financial ruin. Types Of Life Insurance Most people purchase term or whole life insurance policies. Whole life policies are beneficial in that they accrue interest over time. You can take out loans against the money you’ve paid, you can also request the interest you earn be used to pay your monthly premiums. Because they act like a high-interest savings account, you do pay more in premiums. However, they also guarantee that your premium will never change, no matter how old you become. Term insurance policies have a set time frame, often 20 years. For 20 years, you make monthly payments towards your life insurance policy. If you die in those 20 years, your beneficiary receives the face amount. If you don’t, you must renew the policy or find new insurance. The rates will increase because you are older. In addition, most term life policies will not offer life insurance policies to those who are 80 years or older because of the higher risk of dying during the life of the policy. Those that do offer policies will charge exorbitant rates. The exception to this are companies that offer miniscule policy amounts, usually no more than $25,000. Applying For Life Insurance To receive a life insurance policy, you fill out an application. The application asks for basic information, such as: Name Address Date of Birth Gender Marital status History of smoking, drug or alcohol addiction, if applicable Family’s health history Basic health history If your application passes the first round, you will be asked to set up a health exam by the insurance company’s paramedical. That person comes to your house to draw a blood sample, collect a urine sample, measure your blood pressure, get your weight and height and then take your pulse. High policy values may require additional tests like a cardiac stress test and EKG.  Knowing Life Insurance Limitations

Life insurance policy coverage is an insurance policy that is designated to pay a beneficiary a specified amount of money upon the death of the person who is insured. The insurance policy may be secured by someone other than the insured and the beneficiary of the policy may be someone other than the buyer. There are, however exclusions, restrictions and limitations. Most life insurance policies have these that are designed to withhold payments and benefits under certain circumstances. Most life insurance companies will not pay out monies should the insured be involved in certain activities such as high-risk jobs, military action for example. Most life insurance limitations on payout include if the insured commits suicide within a given amount of time after the life insurance policy is purchased. Also, there is a contestability period that the insurance company can challenge the cause of death and may request additional information before agreeing to any payment of life insurance benefits. Other Types Of Life Insurance Limits Companies who provide life insurance policies are allowed to assess a policyholder on a series of things. Some of these criteria used to determine coverage limits are age, gender, height and weight, purpose of insurance, marital status and children and occupational high-risk jobs included. Depending on the answers to the https://www.togelz88.com criteria, your insurance coverage policy amount(s) will be limited as to what is determined by that particular insurance company. When referring to limitations of life insurance policies, the type of policy purchased may also be considered. For example, there are two types of life insurance policies, one is called whole life, which is life insurance covering your life. The expiration date comes once the insured has died and the benefits are paid to their beneficiary. The limited version of whole life insurance is “term” life insurance, which is a life insurance policy purchased for a particular amount of years such as five, ten, 20 and so on. You should discuss these options before purchasing your policy. There are limitations on the amounts of coverage one can purchase. Insurance companies usually have upper limits to policy benefit payouts.  Life Insurance Beginnings

Life insurance has existed in some form or another for millennia. The beginnings of life insurance date back to early Rome, where burial clubs were a popular way of helping members pay for burials and assist the surviving family of the deceased with other expenses. Life insurance in its modern form dates back to England in the 1800s. Lloyd’s of London, then Lloyd’s Coffee House would insure the traders before they left for other countries. Life insurance in America started in the mid-1700s as a financial protection for widows and their children. Most of the insurance companies in America before the Civil War specialized in life insurance for slaves. They were treated like the rest of the property and the owner of the slave would receive the death benefit not the family of the slave. Modern Life Insurance In its modern form, life insurance is used as a way to offer monetary relief to the beneficiaries after the death of a loved one. Today the average funeral can cost is between $6,000 and $7,000. For a family with a modest income, this can entirely wipe out their savings account if they could even afford the cost in the first place. For those who are the primary breadwinner in their family, their death could leave their surviving family financially devastated. Life insurance is vitally important for those with children. It is extremely important to make an effort to continue to support them financially even after death. It is quite common these days to have double-income households which can make life insurance even more important. This can be especially true if the surviving spouse/partner will have to alter their work to care for children. Continued Financial Stability Continuing the financial stability of the surviving family after a death is an important gift. It is so important that many companies offer life insurance as a benefit. Any person can be named as beneficiary. If someone cares for an elderly parent they can name their parent as a beneficiary to insure continued care in the event of the insured party’s untimely death.  With the development of science and technology, man has become to win many things and risks. But it is difficult to overcome or win some things and risks like accidents, reaching to old age and deaths and so on. Though it is impossible for man to defend them but there is invented various types of financial defensive strategies and ways.

These kinds of ways are known as the policies of life insurance. Specialist Benjamin Franklin said that, "Life insurance is a rainbow in a cloudy sky." So we can also defined the life insurance policy as, it is an way of an agreement by signing in a written contract in which we are capable of securing our life financially for a definite period or for entire living age with a good faith and well known insurance company against all of the potential risks of anything horrible incident happens in upcoming days. The importance's of life insurance policy in individual and family life are expressed according www.indotogelx.com in the following below. 1. Relieves the misery caused by death Death is a universal truth event for a man's life for which we say man is mortal. Insurance companies can help financially to the insured peoples families and their members on their financial crisis if that insured is died or unable to bear the family costs. 2. Helpful for old age Reaching to the old age is also a universal truth. Then there are various reasons for money. If anyone has taken a life insurance policy for his life he will get that needed money from his insurer in his old age. 3. Removes the misery resulting from cessation of income When a person's earning power is reduced or totally banned for the causes of diseases, illness, accident, lameness, unemployment, etc. then an insurance company can helps him financially for his taken policy of life insurance. 4. Assistance in creating savings and investment Insurance companies can take parts in the creation of savings by collecting money as premiums from the insured. They can also participates in investments, through the invest of money of the insured that are gotten from the insurer. 5. Increase of mental satisfaction There is an increase of mental satisfaction of the people by taking a policy. So, finally we can say that, actually the importance of life insurance policies in our individual and family life can't be described in writing.  In the competitive world of insurance business, the success of a life insurance company is mainly depends on the numbers of the installments and fixing up the rates of premiums correctly. There are some factors in the governing of the rate of premium in a life insurance company. These are explained in the given below.

1. Proposed insured sum The rate of premium is specially depends on the proposed insured sum in a life insurance policy. If this kind of insured sum is high, then the rate of premium is also generally high. If it is lower, then the rate of premium is also low. 2. Time period of insurance policy The rate of premium is also depends on the time period of the life insurance policy. According to the all right, if the time period of the life insurance policy is for long time then the rate of premium will be lower and if it is for short time then the rate of premium will be higher. 3. Nature of risk To fix up the rate of premium in a life insurance policy, the nature of risks should be bringing in special consideration. Higher risks generally cause higher rates of premiums. If there are lower risks, then the rates of premiums are also being lower. Here some things of the policy taker means insured are noteworthy. These are: the age of the insured, profession, physical condition, character and habit, family history, residence, financial ability, education and standard of living are important that should be considered. 4. Nature of insurance policy The nature of the life insurance policy is also notable to fix up the rate of premium. The premium rates are lower in a whole life insurance policy than in an endowment life insurance policy. Without any profit in an insurance policy there also the rate of premium is higher than in an insurance policy with profit. 5. Investment facilities The money getting from the policy taker as premiums, the life insurance companies can invest them in profitable businesses. If there are good investment facilities, the insurance companies can do their business well and smoothly. 6. Management expenses The management expenses are also plays a vital role in the fixing up the rate of premium. If the expenses are higher then the rate of premium is also be higher. If the expenses are lower then the rate of premium is also lower. Above the factors are really important to fix up the premium rates in a life insurance policy.  There are several classifications of the life insurance policy on the basis of the duration of the policy. Endowment policy is also divided in classes. Three of them are described according www.entbet88.com in the below:

1. Educational annuity policy This kind of life insurance policy is taken for the interest of the children's education. In this policy, a policy taker opens an educational annuity policy for a certain period of time by paying installments to the insurer. After the end of the time of the policy the insurer gives the insured money as educational annuity in a certain frequent time to the kids named in the policy until a certain period. If the policy holder is died before the end of the time of the policy, then there is no need of any installment. In this case, after the death of the policy holder, the insurer will give the full insured money as educational annuity to the children named in the life insurance policy until a certain period. 2. Double endowment policy This kind of policy is similar to the ordinary endowment life insurance policy. But there is a noteworthy difference between them. In a double endowment life insurance policy, if the policy holder is alive after the end of the time of the policy, then the insurer will be bound to pay doubled than the insured money. If an insured is died during the time period of the policy, then his selected nominee will get the insured money only that was agreed in the policy. The duration of these kinds of life insurance policies are between 10 years to 40 years which means long term. 3. Multi purpose policy Multi purpose endowment life insurance policy is a policy in which there is an arrangement, where many purposes of humans lives are taken together within the same policy. There is an opportunity to get a financial certainty and security of the risks of humans deaths, lameness, illness, unemployment, kids educations, daughters marriages and many other matters. But here the rates of premium are generally high. All of the above policies are important to be considering in taking a life insurance policy.  The way of taking financial security against the risks related to death and life is called as the policy of life insurance now-a-days. This is a popular dissimilar business around the whole world as it is a kind of contract between the insured and insurer. So there are shown some essential elements related to the contract and business. There are mainly two types of elements. These are described in the given below.

A. Legal elements:

B. Elements related with insurance business:

Finally we can say that, a contract of a life insurance policy is build up within both types of all elements in the above; we can’t ignore anyone of them. |